Interest rates are top of mind for anyone planning to borrow money in 2026 — whether you’re buying a car, taking out a personal loan, refinancing a mortgage, or financing education. After years of volatility, 2026 interest rate trends are showing signs of stabilization, with some loan categories becoming slightly more affordable and others still reflecting broader economic pressures.

In this post, we’ll break down the average interest rates on the most common types of loans in 2026, what’s driving rate changes, and what borrowers should expect.

🔍 Why Loan Interest Rates Matter in 2026

Loan interest rates determine how much you’ll ultimately pay to borrow money. Higher rates mean larger monthly payments and more interest over the life of the loan. Rates in 2026 are influenced by a mix of Federal Reserve policy, inflation trends, credit markets, and broader economic conditions. For example, the Federal Reserve held its benchmark rate steady early in 2026 after several cuts in 2025, which affects borrowing costs for consumers and businesses alike.

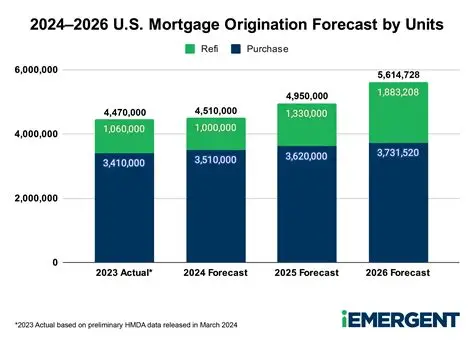

🏡 Mortgage Interest Rates in 2026

Mortgage rates have been a major story for homebuyers and homeowners navigating affordability challenges. As of early 2026:

- 30‑year fixed‑rate mortgages are averaging around 6.1%, remaining near multi‑year lows.

- 15‑year fixed mortgages tend to sit in the mid‑5% range.

These figures are significantly lower than the highs seen in 2024 and 2025, but still above historical averages. For context, long‑term rates have dropped from around 7% a year ago to near 6% today.

👉 For up‑to‑date mortgage interest rate insights, check Forbes Advisor’s mortgage rate guide here: https://www.forbes.com/advisor/mortgages/mortgage‑rates‑01‑30‑26/

🚗 Auto Loan Interest Rates

Car loan interest rates remain higher than the ultra‑low levels seen before the tightening cycle that began in 2022. In 2026:

- New car loans (60‑month): ~7.0% APR

- Used car loans (48‑month): ~7.4% APR

These are averages — your individual rate may vary based on your credit score, loan term, and lender. Borrowers with excellent credit can secure significantly lower APRs.

For a deeper dive into auto loan rates and what’s considered a good rate in 2026, check out this current guide: https://www.alibaba.com/product‑insights/what‑is‑a‑good‑car‑interest‑rate‑in‑2026.html

💼 Personal Loan Interest Rates

Personal loans vary widely because they are often unsecured and based heavily on creditworthiness:

- Average personal loan APR: Around ~12% for well‑qualified borrowers in 2026.

- Some lenders report average APRs ranging from the mid‑teens to over 20% or more for borrowers with weaker credit.

These rates reflect a mix of bank and credit union data as well as marketplace lending trends.

If you want a snapshot of current personal loan interest rates by credit score, explore NerdWallet’s breakdown here: https://www.nerdwallet.com/personal‑loans/learn/average‑personal‑loan‑rates

🎓 Student Loan Interest Rates

Federal student loan rates are set annually and can differ from private student loan APRs. For the 2025‑26 academic cycle, rates on federal undergraduate loans were around 6.39%, with graduate and PLUS loans higher.

Private student loan rates in 2026 vary widely based on credit and lender policies.

📉 What’s Driving These Trends?

So why are these averages what they are?

Economic Policy

The Federal Reserve’s decisions on short‑term rates are central. After cutting rates three times in 2025, the Fed paused early in 2026 to weigh inflation and labor market conditions — a move that influences borrowing costs across the economy.

Inflation & Credit Markets

Inflation has cooled from its peak but remains a factor. Lenders price loans not just on the Fed’s benchmark rate, but on bond markets and risk premiums tied to borrower credit profiles.

Loan Type & Risk

Secured loans (like mortgages and auto loans) usually offer lower rates than unsecured loans (like personal loans) because collateral reduces lender risk.

📊 Bottom Line: What Borrowers Should Know

Here’s a quick snapshot of average loan interest rates in 2026:

| Loan Type | Approx. Average Interest Rate (2026) |

|---|---|

| 30‑yr Mortgage | ~6.1%+ |

| 15‑yr Mortgage | ~5.3%–5.5% |

| New Auto Loan | ~7.0% |

| Used Auto Loan | ~7.4% |

| Personal Loan | ~12% (varies by credit) |

| Student Loan (Federal) | ~6–8% (depending on plan) |

Note: Individual rates vary based on credit score, term, lender, and market conditions.

📌 Final Thoughts

Interest rates in 2026 offer a mixed bag — not dramatically lower than recent years, but easing enough in some categories (like mortgages) to provide relief to borrowers. If you’re planning to take out a loan this year, timing, credit score optimization, and lender comparison can make a meaningful difference in the rate you secure.

🔗 External resources to explore:

- Bankrate’s personal loan forecast for 2026: https://www.bankrate.com/loans/personal‑loans/personal‑loan‑rates‑forecast/

- Auto loan rate forecasts and benchmarks: https://www.bankrate.com/loans/auto‑loans/auto‑loan‑rate‑forecast/

- Up‑to‑date mortgage rate tracking: https://www.forbes.com/advisor/mortgages/mortgage‑rates‑01‑30‑26/